The Life segment comprises the life insurance businesses Pensions, Individual life and Funeral. The segment offers insurance policies that involve asset accumulation, immediate (pension) annuities, asset protection, term life insurance and funeral expenses insurance. Its customers are individual consumers and companies. The market share of Life in 2020 was 14.8% (2019:13.2%) measured in GWP.

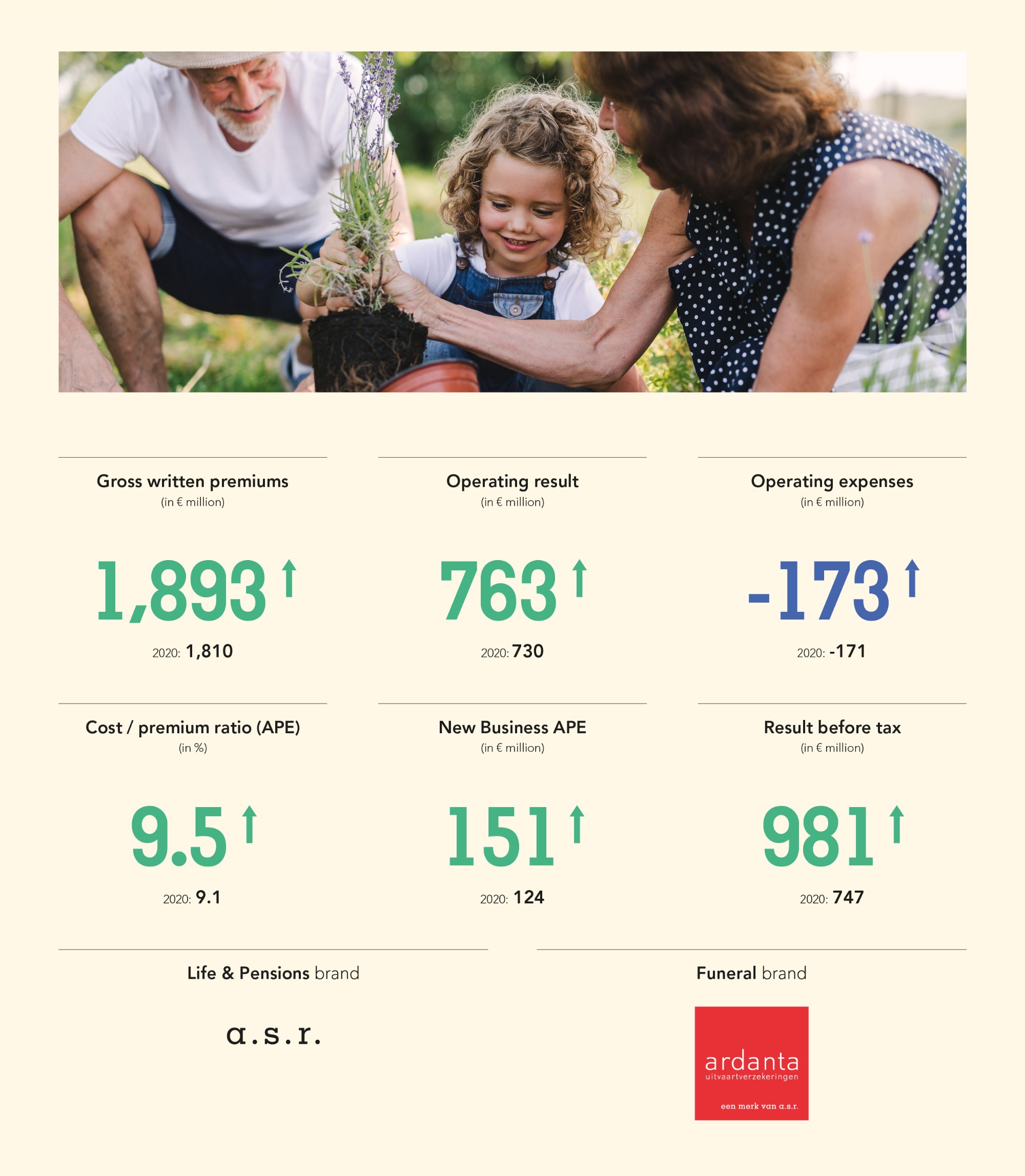

The gross written premiums increased by € 82 million to € 1,893 million (2020: € 1,810 million), mainly due to the strong increase in recurring premiums in defined contribution (DC). The Pensions DC product Werknemers Pensioen (Employee Pension) continued its commercial success this year as the number of active participants increased to almost 130 thousand (2020: almost 104 thousand) and recurring premiums rose by € 172 million (37%) to € 634 million, including the own pension scheme for a.s.r. employees.

The operating result increased by € 33 million to € 763 million (2020: € 730 million), mainly due to the investment margin, which more than offset a decreased technical result.

The investment margin improved by € 62 million to € 682 million (2020: € 620 million), mainly driven by further optimisation of the investment portfolio, resulting in higher investment income and less adverse COVID-19 effects on investment income. Lower dividends from real estate funds, including rental discounts, were partly offset by increased dividend income. The required interest on technical provisions decreased due to the regular run-off in the Individual life portfolio. In addition, the technical result decreased by € 30 million, reflecting lower result on disability cover in pensions as well as the regular run-off of the Individual life portfolio.

The total negative (indicative) impact of COVID-19 was estimated at € 16 million (2020: € 22 million), which primarily reflects lower rental income. The impact on the mortality result is negligible, due to diversification of the various product lines.

The operating expenses increased by € 3 million to € 173 million (2020: € 171 million). The additional cost base from the acquisition of Brand New Day IORP (1 April 2021) and project costs for realising a new IT landscape for the pension portfolio were largely compensated by the efficiency and cost synergies achieved with the completion of insurance portfolio conversions in 2020 (Loyalis and VvAA life) and lower investment charges.

In preparation for the pension reforms, which will take full effect as of 1 January 2027, an important step was taken in selecting a new Software as a Service (SaaS) pension platform. This platform offers customers enhanced digital services and enables a.s.r. to respond more quickly and efficiently to the changing needs of the market while making the administration costs variable.

Life operating expenses, expressed in basis points of the basic Life provision remained stable at 45 bps (2020: 45 bps), which is at the lower end of the target range (45-55 bps) for 2021. Operating expenses in relation to the premiums (measured in APE) amounted to 9.5% (2020 9.1%). This increase is mainly due to the additional cost base from the acquisition of Brand New Day IORP (1 April 2021) and the project costs for realising a new IT landscape for the pension portfolio.

The result before tax increased by € 234 million to € 981 million (2020: € 747 million), driven by an increase in incidental investment income, non-recurring items in 2020 and a higher operating result.

The increase in incidental investment income by € 69 million to € 208 million (2020: € 139 million) reflects the recovery of financial markets this year through positive revaluations. The impact of other incidental items increased by € 132 million and was limited to € 11 million, mainly due to non-recurring items in 2020 related to a goodwill impairment (€ 90 million) and refinement of the calculation methodology for disability insurance in the pension portfolio (€ 33 million).

Life & Pensions

a.s.r. is a major provider of pension insurance in the Netherlands. The defined benefit (DB) product still forms the largest part of the existing pension portfolio, followed by the growing defined contribution (DC) proposition. The current customer base of these portfolios comprises approximately 27,800 companies and 793,000 participants. a.s.r. is the second largest provider of individual life insurance products in the Netherlands, measured in GWP.

With the acquisition of Brand New Day IORP (BND PPI) on 1 April 2021, a.s.r. has strengthened its position on the Dutch pension market, giving substance to its ambition to grow as a provider of capital-light pension solutions. The integration of some parts of BND IORP activities within a.s.r. is expected to be completed in 2022. BND IORP is a separate legal entity and therefore not included in the figures.

The negative indicative impact of COVID-19 on the 2021 operating result of Life & Pensions was limited and mainly concerns lower dividends and rental income. The impact on the mortality result is negligible, due to diversification of the various business lines.

Market

a.s.r. expects the pension market to continue to move from DB to DC solutions in the coming years. With the acquisition of BND PPI, a.s.r. has further expanded its product range in DC solutions.

The switch from DB to DC gives rise to a shift in risk from employer to employee / participant. This switch also leads to declining cost coverage in the market. a.s.r. is taking further steps to enable digital self-service, given that customers expect to be able to arrange their financial affairs online.

Products

a.s.r. provides DC pension products with recurring premiums, in which benefits are based on investment returns on selected funds, in some cases with guarantees. a.s.r.’s DC proposition concerns the employee pension product Werknemers Pensioen (WnP). In 2021, the WnP had almost 130,000 active participants and € 3.0 billion in AuM all invested in SRI funds. The number of active participants at BND PPI grew to 120,000 and the invested capital to € 1.9 billion. In addition to the fixed annuity product, a.s.r. also has the variable pension product. This offers customers a product for the payout phase of their pension, with an appropriate balance between risk and return. a.s.r. also offered DB products, but due to market changes these products are no longer (actively) sold.

Term life insurance, the sole individual life proposition actively sold, consists of traditional life insurance policies which pay out death benefits without a savings or investment feature. a.s.r.’s term life insurance products are mainly sold in combination with mortgage loans or investment accounts, and generally require recurring premium payments. All other individual life products are managed as a closed service book.

Strategy and achievements

In 2021, Life & Pensions launched the Ik denk vooruit platform, which helps customers to improve their financial health and provides more insight into their financial situation, in order to take the right financial decisions. Via the platform, customers have an opportunity to register for the targeted investment product, with which they can choose between three sustainable ASR Vooruit mixed funds.

The competitive position is strengthened through the creation of further economies of scale and a focus on digital transformation and consolidation opportunities.

The Life & Pensions strategy is focused on:

Serving the needs of its clients. Excellent operational performance with a high client satisfaction, data driven orientation and compliance with legislation.

Realising growth by having the right product propositions in place for further growth and looking for opportunities in ongoing market consolidation to acquire portfolios or companies.

Drawing the attention of new and existing customers to the Ik denk vooruit platform, to help customers increase their financial health, providing more insight into their financial situation and helping them to make the right financial decisions.

Realising a new IT landscape to administer the pension portfolio. This new target IT landscape will contribute to the efficient implementation of changes in laws and regulations (among which the new pension legislation) and to further reduce costs.

Continuing with the digitalisation and optimisation of the processes.

NPS-c Life & Pensions

(-100 to +100)

The average NPS-c rating during 2021 was slightly below the 2020 level, due to a temporary decrease in customer satisfaction in the first half of 2021 following longer lead times on policy holder requests. In the second half of 2021 the NPS-c ratings improved again well above target level.

Outlook for 2022

In 2022, a.s.r. will focus on further growth in WnP and immediate fixed and variable pension annuities as well as on further improving customer satisfaction. The implementation of the new Dutch pension agreement has been postponed for a year. a.s.r. will start the implementation after the proposal is debated in the House of Representatives in the spring of 2022. This pension agreement is the result of extensive discussions between government, employers and employees. The agreement is fully in line with the strategy of phasing out DB products and accelerating growth in DC. The outcome of pensions will be more uncertain for individual customers. For this reason, a.s.r. aims to help customers make better financial decisions through the launch of the Ik denk vooruit platform at the end of 2021.

a.s.r. split the L&P activities per 1 March 2022, the management of the (customer service) of Life, the ASR Pensioenfondsen Services (APFS) activities and Funeral are combined. The services books of Life, Funeral and the APFS portfolios (except the Pensions DB portfolio) are also combined. Pensions can focus entirely on (organic) growth and the migration and investments to a new target landscape.

Funeral

As at 31 December 2021, the funeral portfolio of Ardanta, a.s.r.’s funeral brand, consisted of 6.2 million policies and 3.6 million customers. Based on the volume of premiums, Ardanta is the third largest funeral insurer in the Netherlands. The impact of COVID-19 on the 2021 operating result of Funeral was limited because the increased mortality occurred mainly in the higher age categories. COVID-19 had little impact on the payment behaviour of Funeral customers in 2021 see (chapter 6.1.2). Due to the COVID-19 related measures, employees largely served customers from home in 2021. This did not lead to a negative effect on service levels or customer satisfaction.

Market

In recent years, there has been a significant degree of consolidation in this market. Also in 2021, as the acquisition of Yarden by Dela was announced. This acquisition further reduces the number of active providers of funeral insurance, the largest peers of a.s.r. are Dela and Monuta. The consolidation in the funeral insurance market is expected to slow down in the coming years, however a.s.r. does continue to search for opportunities.

Products

Ardanta's primary objective is to insure funeral expenses. Since September 2021, with the introduction of the Ardanta funeral insurance product, Ardanta only offers a capital insurance product. This new product is a modern and comprehensive funeral insurance. It is a flexible insurance policy for which customers determine for themselves how long they wish to pay premiums (minimum of five years, maximum age of 85). There are also many options for retaining the value of the insured sum: the customer can opt to follow the price index figure or for an annual increase by 2 to 5%. Choices can be changed during the term of the policy on the basis of new customer requirements and / or insights. The free choice of undertaker is also important. The customer determines who provides the funeral and the payee for the benefits.

Strategy and achievements

Ardanta focuses on the provision of good and innovative services to its customers. The 100% digital programme was launched in 2019. This digital transformation involves a fundamental change in customer interaction, value propositions, business models, operational processes and customer experience. The initial results of the digitisation of the advisor process and the process for digital contracting of new insurance policies were positive. The conventional form, in which customers and advisors contact Ardanta (by telephone and mail) is diminishing. In 2021, digital services accounted for 55% of Ardanta’s outgoing annual output. Customer satisfaction (NPS-c) remained stable at 47 in 2021 (2020: 47). Ardanta also offers practical guidance to its customers and their relatives on matters relating to bereavement, through initiatives such as a funeral coach, who assists relatives in the days immediately after a relative has died.

NPS-c Funeral

(-100 to +100)

Ardanta continues to focus on capital generation and the further strengthening of its competitive position. Efficient operations, reflected in the costs per policy, form an important driver for this. Ardanta’s distinguished proposition is recognised in the market: organic growth targets were exceeded in 2021 in both the traditional intermediary channel and in direct distribution channels (internet, direct mail and own advisors).

Ardanta’s sustainability initiatives focus on address enrichment in order to re-establish contact with customers which were lost over the decades. In addition, an active search is conducted to trace the relatives of long-deceased customers in order to settle outstanding financial entitlements.

Outlook for 2022

Whilst taking into consideration the volume of a.s.r.’s funeral portfolio there is still potential for organic growth. The customer contact strategy will be further developed resulting in new marketing campaigns focused on digital access for customers. The aim is to create awareness amongst customers of their existing insurance asking them to check whether this is still appropriate.

Aligned with a.s.r.’s digital strategy, the digitisation programme will continue. In 2022, the focus will be the processes relating to existing customers and on activating customers to do business digitally. With this continuing digitisation, special attention will be devoted to vulnerable groups, such as those with low literacy and those without digital devices.

Inclusive funeral insurancea.s.r. promotes equal opportunities for all; internally, a.s.r. uses the Diversity, equality and inclusion policy to that end. Externally, a.s.r. contributes to an inclusive society wherever possible.

Since July 2021, people who are under guardianship can take out funeral insurance at Ardanta without any thresholds or health questions. When applying for funeral insurance, medical questions are always asked. This vulnerable group of people is often asked additional questions. This is a time-consuming and complex process for this group, which is why they often do not take out insurance.

Ardanta developed a collective scheme that makes it easy for people under guardianship to insure themselves against funeral costs. The scheme is intended for administrators’ customers who live at home or in a small-scale residential facility. The NBBI, the trade association for administrators, reacted enthusiastically to Ardanta’s initiative and is publicising the collective scheme within its branch.